Chris is an award-winning former journalist with 15 years of experience in the mortgage industry. A national expert in VA lending and author of “The Book on VA Loans,” Chris has been featured in The New York Times, the Wall Street Journal and more.

Updated on November 3, 2023 Veterans: Check your $0 down eligibility today! Expert Reviewed At a GlanceAssuming another's VA loan is an intriguing benefit with VA loans. Here we take a look at what an assumption is, the process and who can assume a VA loan.

One of the under-the-radar benefits of VA loans is that they're assumable. That hasn't meant much in recent years, with mortgage rates at modern-day lows.

But with today's higher rates, the ability to essentially take over someone else's mortgage -- including their low interest rate and monthly payment -- is a huge opportunity.

With a VA loan assumption, you are inheriting a Veteran's active mortgage. You don't have to be a Veteran to assume a VA loan, although there are some risks involved for Veteran homeowners who allow civilians to take over their mortgage (more on that later).

Loan assumptions and traditional home purchases differ in some fundamental ways.

They can make homeownership more affordable for would-be buyers and give VA homeowners a big bargaining chip when it comes to marketing their home listing. Assumptions feature fewer costs and fees than traditional purchase loans.

Like every mortgage tool, loan assumptions come with both benefits and drawbacks. First, let's take a look at the potential benefits of a VA loan assumption.

Yes, VA loans are assumable. For prospective buyers, the ability to assume a VA loan with a low interest rate is a significant benefit when rates are on the rise. But assumptions can also present some risks for the Veteran allowing their loan to be assumed.

For prospective buyers, the two biggest benefits of a loan assumption are rooted in cost savings. An assumption means you can take advantage of the low rate a homebuyer locked down months or even years prior, when the housing market looked a lot different.

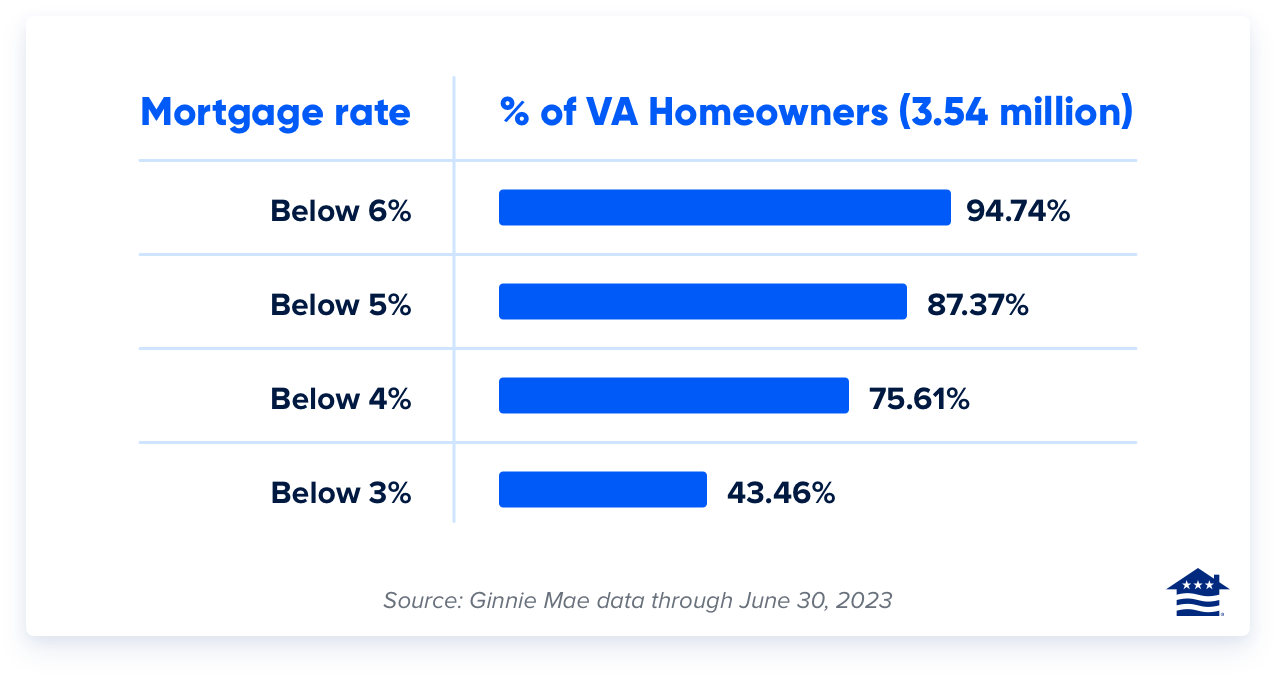

Nearly 90% of VA homeowners have a mortgage rate below 5%, according to a Veterans United analysis of Ginnie Mae data through June:

It's tough to overstate the impact of those lower rates on housing affordability.

On a $400,000 loan with a 7% interest rate, the monthly principal and interest payment comes out to about $2,660. With a 3% rate, that payment drops to $1,686. That's nearly a thousand-dollar difference in monthly housing costs.

Would-be buyers can't get a rate anywhere close to that 3-5% range right now.

The other money-saving benefit of a VA loan assumption is that they come with few costs and fees, especially compared to a traditional purchase loan. Most of the closing costs associated with a VA purchase aren't part of an assumption.

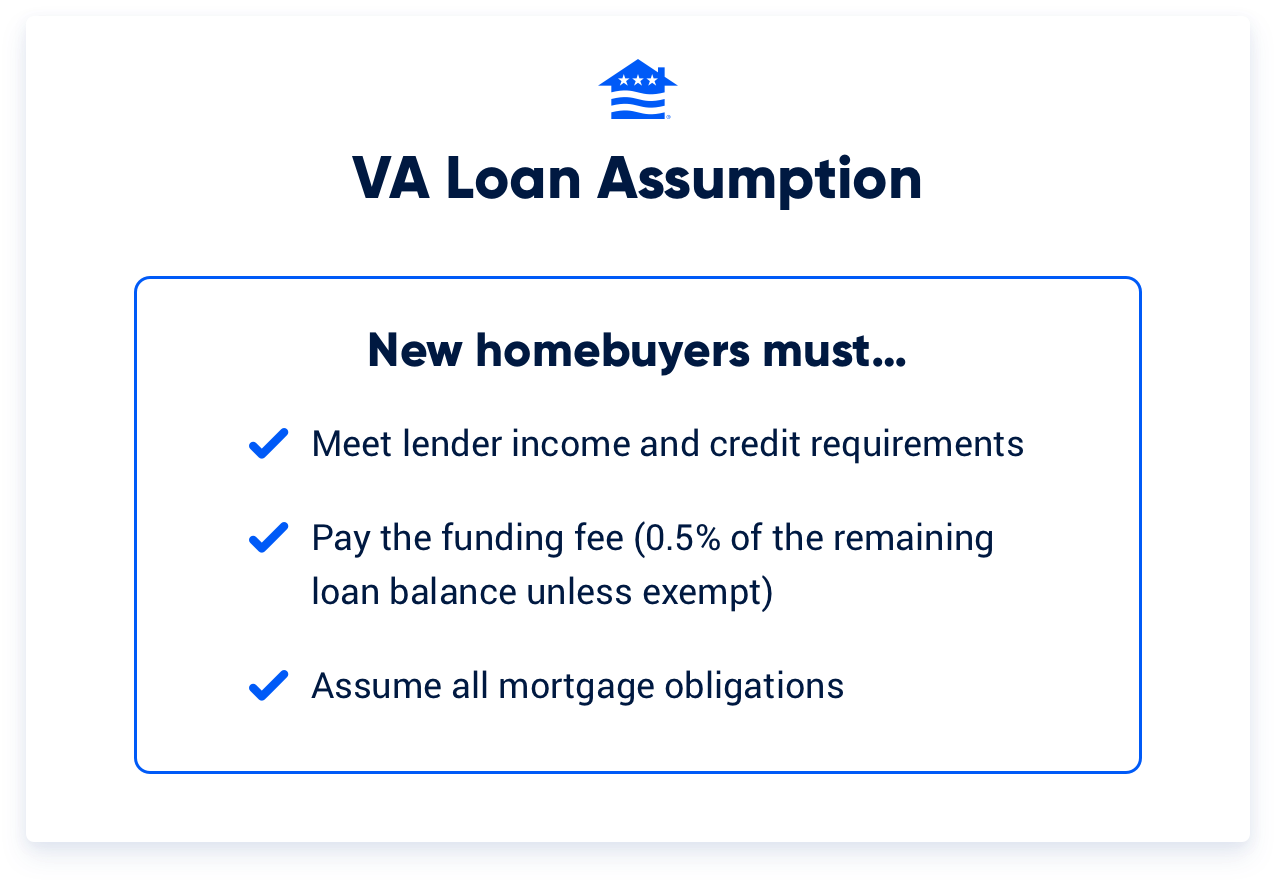

The person assuming the loan does pay a funding fee of 0.5 percent of the loan balance. That fee goes directly to the VA and helps keep the loan program running for future generations of military buyers. Veterans who would typically be exempt from the VA Funding Fee are also exempt from this assumption fee.

Loan assumers might also want to pay for an appraisal, but those aren't required with loan assumptions.

Yes, VA loans can be assumed regardless of whether you're a Veteran. But there's risk involved for VA homeowners who allow for assumptions to civilians.

Now let's take a look at some of the challenges of a VA loan assumption. There's one big one for prospective buyers and one facing VA homeowners.

Would-be buyers don't just waltz in and take over a Veteran's mortgage without paying for the privilege. Homeowners want to make sure they capture whatever equity they've built in the property, otherwise there's no benefit to allowing for an assumption.

For example, let's say the VA homeowner has $350,000 remaining on their loan, and they're selling their home for $450,000. The person assuming the loan would need to pay the homeowner $100,000 at closing in order for an assumption to make sense.

In most cases, loan assumers cover that cost in cash, which can be a tall order for some consumers. But it might be possible to obtain secondary financing to pay out the homeowner's equity at closing. Lenders will likely include that debt when they consider a loan assumer's overall debt and income situation.

In either case, would-be buyers need to figure out how they'll cash out the homeowner's equity in order to make a VA loan assumption work.

For VA homeowners, the big consideration with allowing an assumption is their VA loan entitlement. If the person assuming your loan is a Veteran with sufficient VA loan entitlement, then you can ask them to formally substitute their entitlement for yours on that mortgage. Otherwise, the entitlement you utilized to purchase the home will remain tied up there until the loan is fully repaid.

Failing to get a substitution of entitlement can limit your 0% down purchasing power when it comes time to reuse the VA loan benefit. It's also possible you wouldn't have enough entitlement remaining to reuse the benefit at all.

VA homeowners also lose that portion of their entitlement entirely if the assumer later experiences a foreclosure or short sale.

In other words, allowing a civilian to assume your VA loan can affect your future use of the VA loan benefit. For some homeowners, that's a risk worth taking. Others ultimately decide to allow for assumptions only to Veterans substituting entitlement or to pursue a traditional home sale.

There are a few different ways you can find assumable VA mortgages. The first is to work with a real estate agent and ask them to locate homes with assumable VA loans. Working with an agent who has access to the multiple listing service (MLS) will make shopping for homes with assumable mortgages much easier.

Another way you can go about finding assumable VA loans is to search individual home listings on the major real estate search sites. Some home sellers advertise their assumable mortgage to help their listing stand out.

Veterans and civilians who want to assume a VA loan first need to find them. A good real estate agent can help, but home listings on major sites are increasingly referencing assumability as a major benefit.

Generally, a home with a VA or FHA loan is assumable. Conventional mortgages in most cases are not.

The VA has broad assumption guidelines. Lenders and servicers holding these loans will likely have their own unique requirements that would-be assumers must meet.

Guidelines and requirements might include:

If you're looking for an assumption, you'll be dealing with the lender or servicer that made the original VA loan. Lending guidelines, processes and time lines will vary.

Veterans United’s VA loans are assumable, but not all loan types offered by Veterans United have assumability. Borrowers with VA loans through Veterans United have the option to transfer their loans to another eligible individual, subject to VA approval. However, assumability does not apply to other loan types offered by Veterans United, such as conventional and FHA loans.

See What You Qualify ForAnswer a few questions below to speak with a specialist about what your military service has earned you.

Chris Birk is the author of “The Book on VA Loans: An Essential Guide to Maximizing Your Home Loan Benefits.” An award-winning former journalist, Chris writes about mortgages and homebuying for a host of sites and publications. His analysis and articles have appeared at The New York Times, the Wall Street Journal, USA Today, ABC News, CBS News, Military.com and more. More than 300,000 people follow VA Loans Insider, his interactive VA loan community on Facebook.

About Our Editorial Process

Veterans United is recognized as the leading VA lender in the nation, unmatched in our specialization and expertise in VA loans. Our strict adherence to accuracy and the highest editorial standards guarantees our information is based on thoroughly vetted, unbiased research. Committed to excellence, we offer guidance to our nation's Veterans, ensuring their homebuying experience is informed, seamless and secured with integrity.

The VA funding fee is a governmental fee required for many VA borrowers. However, some Veterans are exempt, and the fee varies by VA loan usage and other factors. Here we explore the ins and outs of the VA funding fee, current charts, who's exempt and a handful of unique scenarios.

Can Your Mortgage Be Denied After Preapproval? Updated on April 15, 2024It is possible for you to get denied for a home loan after being preapproved. Find out why this may happen and what you can do to prevent it.