There are countless reasons as to why an entrepreneur would prefer to raise funds through a private placement rather than another form of financing. For example, a private placement allows a firm to remain private and not worry about meeting the many regulatory requirements (including costs and disclosures) that a typical Initial Public Offering (IPO) would require. In addition, the process is speedier and allows an entrepreneur to work exclusively with accredited investors, if the entrepreneur so chooses.

A critical document involved in private placements is the private placement memorandum (PPM) or offering memorandum. Private placements and the memorandum will be discussed at length throughout this blog post.

A private placement is a sale of stocks, bonds or other securities directly to private investors. A private placement offering is an unregistered securities offering and is covered under SEC Regulation D of the Securities Act (Rule 504, Rule 506(b) and Rule 506(c)).

A common disclosure requirement, in practice, for private placements is the private placement memorandum. Under Rule 506(b) and Rule 506(c) a private placement memorandum is not required; however, under Rule 506(b) it is highly recommended that an issuer (entrepreneur) create a private placement memorandum because non-accredited investors are a part of the offering. The private placement memorandum is a securities disclosure document. The document is a comprehensive assessment of the business’s operations, financial position, legal issues, etc.

The objective of the private placement memorandum is to provide future investors with sufficient information so that investors can perform an adequate analysis of the business and decide whether to invest in the company.

Typically, the company's management team along with his investment bankers and attorneys will craft the private placement memorandum. It's important to ensure the risk section is adequate to protect both the issuer and the investors.

If the issuer is an independent sponsor or self-funded searcher, they may elect to prepare the PPM with outside counsel or a platform like Mainshares, instead of a lower-middle market investment bank. In this case, they will likely base their PPM on similar disclosure documents and work to flush out the document before formally approaching investors.

When the issuer is ready to approach investors to finance their deal, they will likely start outreach with an email blurb and follow it with a short teaser. The short, anonymized teaser helps investors decide whether the transaction fits their “buy-box.”

If the transaction fits within the investment focus of an investor, the next step is typically the execution of a non-disclosure agreement after which the private placement memorandum is shared.

The PPM is important for entrepreneurs because it protects them on the regulatory front. Unlike a short deck that may only pitch the upside of a transaction, a private placement memorandum does a good job of outlining transaction risks, governance rules, and other considerations for investors to consider.

This ensures that investors are backing you with their eyes wide open and that there are no accusations of negligence or omission of key risks down the line.

A common Private Placement Memorandum includes an executive summary, description of the business and the security offered for sale, terms of the sale/agreement, capital structure and historical financial statements, biographies of executive management, and numerous risk factors associated with the investment (i.e., risk factors specific to the sector, industry and firm).

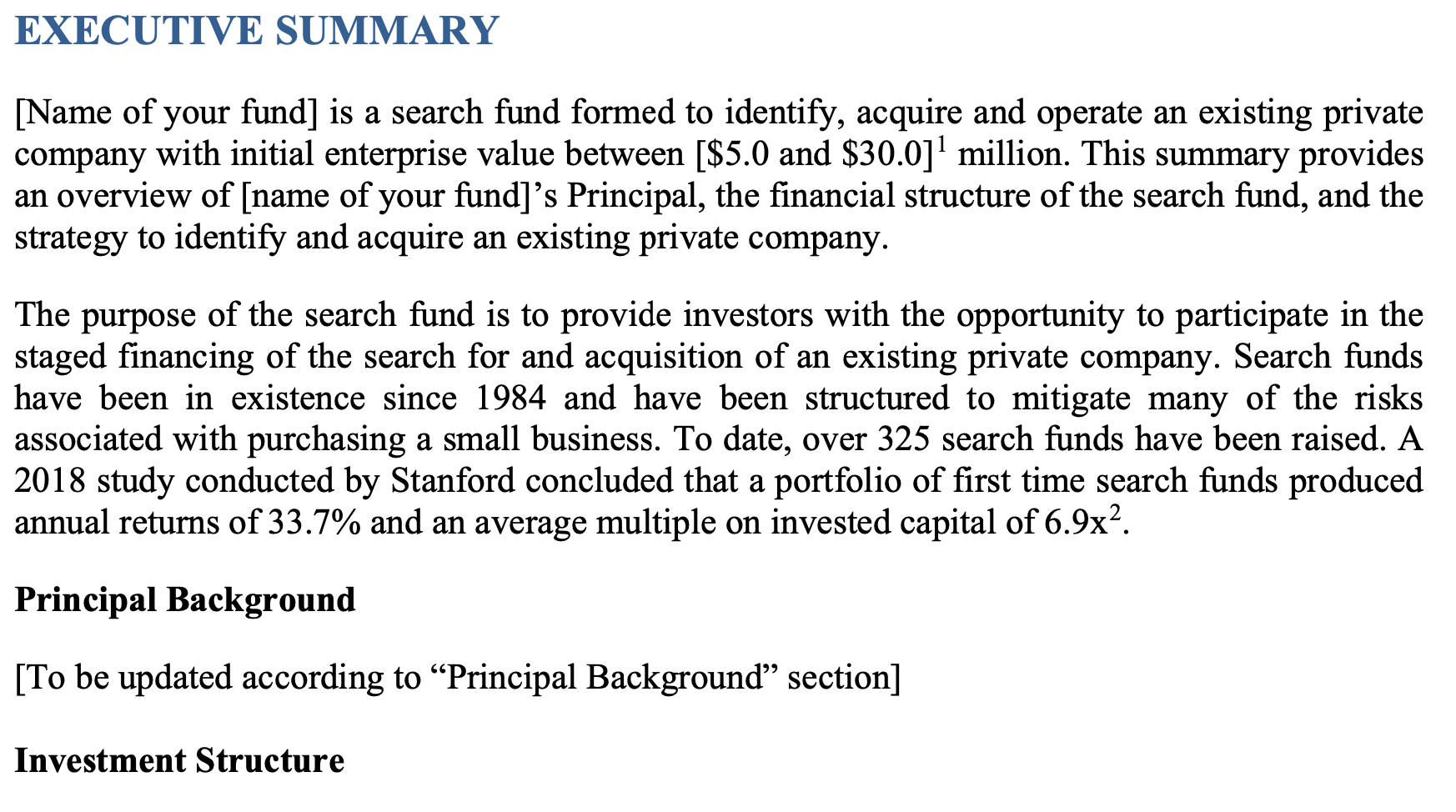

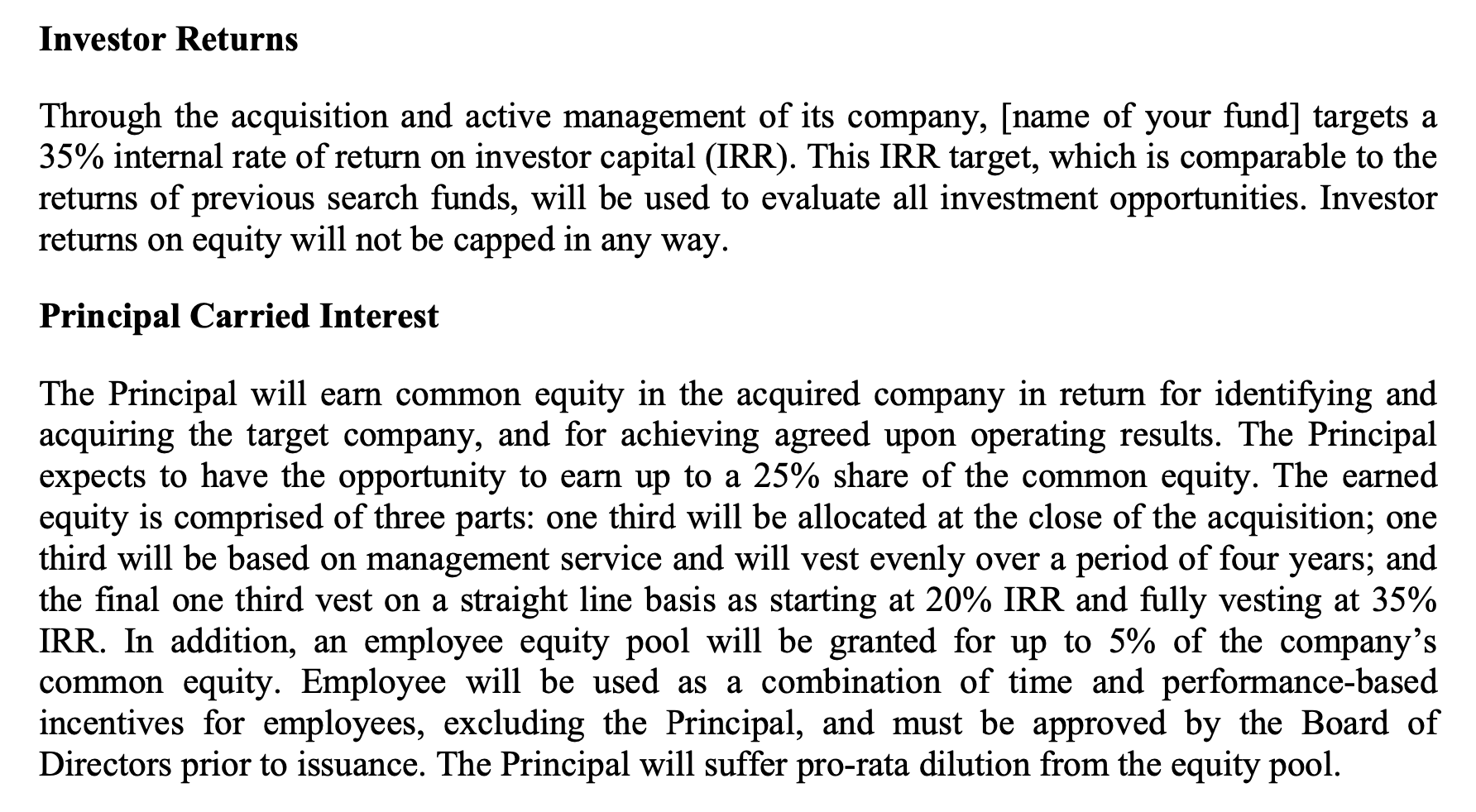

The executive summary starts with details about the firms involved in the private placement and then describes the background of the issuing firm. An overarching goal in this section of the private placement is to give investors an overview of the transaction, the high level structure of the investment and details on the market and opportunities.

Below is sample language used for a traditional search fund:

Arguably the most important section of the private placement memorandum for companies raising growth capital, this section details the capital structure and financial history of the firm. Oftentimes detailing past successes and failures of the firm and trend analysis of the firm's financial statements. Material information, such as past mergers and acquisitions, capital raises, debt offerings, etc, and its successes and failures will be detailed in this section.

This section will likely not exist in the PPM for a traditional search fund, but the PPM for a self-funded acquisition, where the acquisition target has already been identified, will include information on the capital structure of the target and its historic financials.

In this section, depending on the size of the management team, an issuer may only have executive management’s biographies. Within the biographies, an issuer details how long the individual has been with the firm and the career history of that individual. This section is straightforward and allows investors to get to know who is operating the firm. Lastly, the section wraps up with details about the ownership structure. For example, is the firm a parent company and operates as a conglomerate, or is the firm an LLC, LP, etc.

For self-funded or traditional search funds, this will obviously include the searchers themselves and may also include any advisors or board that has been formed.

This section will include the details of a private placement's offering to investors. The details cover distributions, the terms of the sale, the amount of money that will be raised through the private placement, what the funds will be used for and common governance clauses. In short, the summary of terms agreement section details why the issuer is raising funds, what those funds will be used for and how the investment will be managed.

Below is a template of part of the summary of terms for a traditional search:

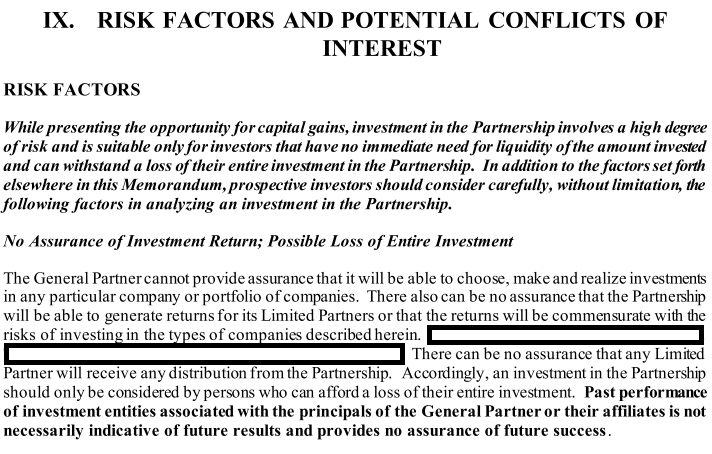

The last important section of a private placement memorandum is the numerous risk factors section. The section is used to detail the risk factors involved in the transaction, industry and sector. In essence, investors must read this section with great detail because this is the risk that investors will be compensated for. Typical risk factors included financial market fluctuations, investments in foreign countries, middle market firms, no assurance of investment returns, competitive marketplace, etc.

In short, the numerous risk factors section is one way an issuer can protect themselves from a legality perspective. Since the pandemic has passed, it wouldn’t be surprising if in this section the issuer discusses how future pandemics may affect the firm.

Below is an example from the numerous risk factors section:

It is important to note that each private placement memorandum is different and highly dependent on the sector, industry and firm. Moreover, private placements come with a high amount of risk due to their speculative and illiquid nature; therefore, it is imperative that issuers and investors consult with legal counsel and other experts before issuing or investing in a private placement.

Information posted on this page is not intended to be, and should not be construed as tax, legal, investment or accounting advice. You should consult your own tax, legal, investment and accounting advisors before engaging in any transaction.

Join our bi-weekly SMB newsletter. It's free and not annoying.

© 2024 Mainshares, LLC. All rights reserved. Disclosure:This website (the “Website”) is owned and operated by Mainshares, LLC (“Mainshares”). By accessing the Website and any pages thereof, you agree to be bound by Mainshares’ Terms of Service and Privacy Policy, as well as the Terms of Service and Privacy Policy for Main Street Securities, LLC (“Main Street”). The information contained herein is provided for informational purposes only and is not intended to influence any investment decision or be a recommendation for any investment, service, product, or other advice of any kind, and shall not constitute or imply an offer of any kind. The products and services offered by Mainshares are not offered by a certified public accountant (“CPA”) and should not be considered as a substitute for services provided by a CPA.

The information contained herein is provided by Mainshares, LLC (“Mainshares”) for informational purposes only and is not intended to influence any investment decision or be a recommendation for any investment, service, product, or other advice of any kind, and shall not constitute or imply an offer of any kind. The products and services offered by Mainshares are not offered by a certified public accountant (“CPA”) and should not be considered as a substitute for services provided by a CPA.

Broker-dealer services provided in connection with some of the investment opportunities on the Mainshares platform are offered through Main Street, a registered broker-dealer, affiliate of Mainshares, and member of FINRA/SIPC. For additional information, please contact your licensed securities representative of Main Street Securities LLC or visit FINRA’s BrokerCheck. If the investment opportunity does not include the "Brokered by Main Street Securities" designation, broker-dealer services were not provided in connection with the offering through Main Street.

Neither Mainshares nor Main Street Securities LLC make investment recommendations and no communication, through this Website or in any other medium should be construed as a recommendation for any security offered.

Should you be presented with an investment opportunity, such investment opportunities involve private, unregistered securities that are speculative and involve substantial risk. These investment opportunities are conducted in accordance with an exemption from registration, specifically relying on the private offering provision outlined in Section 4(a)(2) of the Securities Act of 1933, along with compliance with Rule 506 of Regulation D. All investments involve risk and the past performance of a security, or financial product does not guarantee future results or returns. There is always potential to lose money when you invest in securities or other financial products. Private placements lack liquidity and distributions are not guaranteed. You are strongly encouraged to seek professional advice prior to entering into any transaction for any securities and to consider your investment objectives and risks carefully before investing.

Neither the SEC nor any federal or state securities commission or regulatory authority has recommended or approved any investment or the accuracy or completeness of any of the information or materials provided herein or through any references/links herein. There can be no assurance that any valuations provided by issuers are accurate or in agreement with market or industry valuations. Neither Mainshares nor Main Street Securities LLC make any representations or warranties as to the accuracy of such information.